Strategy

Why is Australia’s Financial Year from July to June?

Small business owners scramble in May and June to get everything wrapped up for the End of Financial Year. But why is it the end of the year for businesses halfway through the calendar year?

The Australian tax year, the financial year runs from July 1 to June 30. The timing seems odd but the purpose is to align financial activities with government operations, which makes it smoother to manage and report tax obligations and financial statements.

While it is essential that business owners understand this offbeat cycle for legal reasons, individual taxpayers need to understand how this works too as it will dictate when to prepare and submit financial reports as well as personal tax returns.

Since the Commonwealth’s establishment in 1901, Australia has adhered to the July to June fiscal calendar. The rationale for aligning the financial year with these dates was practical. Historically the Australian Parliament sits in May and June so these dates made it convenient to pass a budget during this time, while meetings in November and December presented challenges around the festive season. When you think about it, trying to wrap up your business paperwork around public holidays and time with your family isn’t that appealing anyway.

Like it or not, to meet legal requirements your financial planning and business decision-making need to revolve around this timeframe, which is going to require a well-organised financial management system. Here’s how to get it right:

Contents

History of the Australian financial year dates

The financial year we have today is a frame for government accounting, taxation and financial matters. Different Australian states originally had their own financial year settings, most based close to the British system ending on the 5th of April. In the late 1800’s States adopted changes one by one to end June 30. The current financial year became unanimous Australia-wide with the newly formed Commonwealth of Australia federation in 1901.

The decision for June aligned with fiscal policies and the needs of the government, establishing a consistent period for Australia’s economic management once and for all.

Understanding the Australian tax year

Understanding the Australian Financial Year (FY) will help with tax planning and financial management. Once you start thinking about a business year as being different from the calendar year things start to get easier. If you only use the fiscal year for thinking about tax, it’s going to create some conflict around your business discussions and planning. Just use the fiscal year for everything related to your business and make it really clear-cut.

In Australia, the financial year—(FY)—is the period used for organising taxation and financial statements. It starts on 1 July and concludes on the next year’s 30 June. Small businesses need to maintain financial year compliance ATO standards to comply with the Australian Taxation Office (ATO) by meeting these deadlines, so it can be really beneficial to align your business operations with the fiscal year.

Make sure you get familiar with the labels to help with financial planning and analysis (as well as looking like you know what you are doing). In documents and reports, the financial year is abbreviated. FY2024, for instance, designates the period from 1 July 2023 to 30 June 2024, and it can also appear as FY23/24.

Here’s how the financial year influences your business activities:

- Tax preparation: You need to report your earnings and expenses within this timeframe.

- Tax benefits: As the financial year winds down, strategic purchases could be made to optimise your tax position.

- Budgeting: It’s a standardised cycle for setting and reviewing budgets.

- Comparison of Performance: Aligning with FY dates allows for straightforward comparison with prior years, helping you understand your business trajectory.

- Annual Budget Cycle: The Australian government releases its budget typically in May, which influences your strategic planning. It gives you the chance to adjust to new financial conditions before the fiscal year begins.

- National Minimum Wage: Set by the Fair Work Commission, these adjustments usually come into effect at the start of the financial year.

Remember, these dates are critical for ATO compliance and to ensure the accuracy of your financial reports. Knowing the period of the financial year empowers you to manage business finances well. The FY2024 financial year in Australia, for instance, designates the period from 1 July 2023 to 30 June 2024.

Current Financial Year Key Dates

Managing your financial year compliance ATO requirements is much easier when you have the major deadlines mapped out. These are the dates to circle in your calendar:

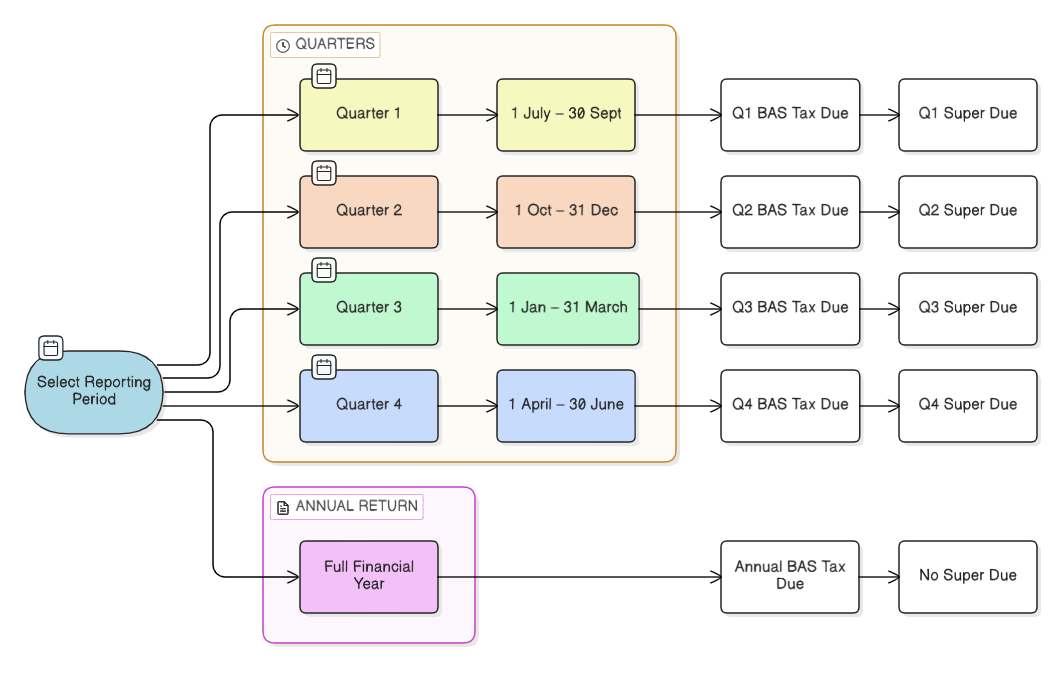

Quarterly Activity Statements (BAS): For most small businesses, your Business Activity Statements are due on the 28th of the month following the end of the quarter:

- Quarter 1 (July–Sept): 28 October

- Quarter 2 (Oct–Dec): 28 February

- Quarter 3 (Jan–March): 28 April

- Quarter 4 (April–June): 28 July

If you use a registered tax or BAS agent, you may be eligible for an automatic extension (concession) for the Quarter 1, 3, and 4 deadlines, often giving you an extra four weeks to lodge.

Annual Income Tax Returns: The EOFY tax deadline Australia for your annual return depends on how you choose to lodge:

- 31 October: The standard deadline if you are self-preparing and lodging through myTax.

- 15 May (Following Year): The typical extended deadline if you are using a registered tax agent (provided you are on their client list by 31 October).

Superannuation Guarantee (SG): To ensure you can claim a tax deduction for your employees’ super, payments must be received by their fund by:

28 October, 28 January, 28 April, and 28 July.

Taxation Laws and the EOFY tax deadline Australia

Taxation laws often require financial reports and adhering to the Australian financial year ensures your compliance. It simplifies your process by giving you a fixed period to prepare documents and make informed financial decisions.

By maintaining financial records from July to June, you can provide accurate reports which are essential for tax assessments, business evaluations, and strategic planning. Remember that meeting the Australian EOFY tax deadlines is vital for avoiding penalties and maintaining good standing with regulators.

Business Planning and financial year compliance ATO

The period from July 1 to June 30 is significant for you as a business owner in Australia because it aligns with The Business Activity Statement (BAS), which reports Goods and Services Tax (GST), pay-as-you-go (PAYG) instalments, PAYG withholding tax, and other taxes, which must be submitted quarterly or monthly, depending on the business size and requirements.

Small business tax can often be forgotten in the day-to-day running of a business, so plan ahead and be ready to pay on time so it’s not cutting into your personal funds (or leaving you in debt) at tax time. To ensure total financial year compliance ATO guidelines must be followed regarding GST and PAYG withholding.

Tax Planning: By recognising that the fiscal year ends in June, you can better schedule your activities to maximise tax advantages. Consider the timing of major purchases or income deferral to the next financial year to manage tax liabilities.

- Income: Deferring income to the next fiscal period might lower your taxable income for the current year.

- Expenses: Accelerate deductions by purchasing necessary equipment before year-end to claim depreciation.

Reporting and Forecasting: Align your reporting with the financial year for a smooth process. Use historical data from the same period to predict trends and set realistic targets for performance and growth.

- Quarterly Reviews: Track your progress to identify strategies that are working and those that require attention.

- Annual Projections: Develop forecasts based on the previous year’s performance to guide your strategic objectives.

Incorporating Knowledge of the Financial Year:

- Adjust business plans in response to tax changes before July 1.

- Leverage fiscal year timelines for budget preparation.

- Employ strategic tax positioning within the definitive fiscal year frame.

By syncing your strategies with the financial year, you set a solid foundation for your business to thrive.

| Strategic Pillar | Practical Action Item | Business Impact |

| Tax Preparation | Report all earnings and expenses within the July 1 – June 30 window. | Ensures financial year compliance ATO standards are met and avoids late penalties. |

| Tax Benefits | Review the FY2024 financial year Australia assets and make strategic purchases before June 30. | Optimizes your tax position through deductions like the “Instant Asset Write-off” (for eligible assets under $20,000). |

| Budgeting | Use the standardized July–June cycle to set annual financial targets. | Creates a predictable rhythm for cash flow management and resource allocation. |

| Performance Comparison | Align internal data with Australian financial year dates to compare against prior years. | Provides a clear “business trajectory” by comparing consistent 12-month data blocks. |

| Annual Budget Cycle | Review the Federal Budget (released in May 2026) to adjust for new government policies. | Allows you to pivot your strategy in response to new grants or tax changes before the new year starts. |

| National Minimum Wage | Update payroll systems for the Fair Work Commission’s annual wage increase (effective 1 July). | Ensures legal compliance with new pay rates and protects you from underpayment claims. |

Need help with your business finances? Here’s why a business mentor makes a difference.

What can small businesses do to get ready for June 30?

Small businesses can do several things to prepare for the end of the financial year, ensuring they meet compliance requirements and possibly maximise returns. Here’s a checklist to get ready:

- Organise Financial Records: Keep accurate and organised records including invoices, receipts, bank statements, and payroll records. A clear record of income and expenses will streamline the tax filing process.

- Review Tax Deductions: Understand what expenses can be deducted from your taxable income, such as business supplies, travel expenses, and certain types of business insurance. Taking advantage of all eligible deductions can significantly reduce your taxable income.

- Update Accounting Software: If you use accounting software, make sure it’s updated to the latest version to tap into new features and be compliant with current tax laws.

- Prepare Financial Statements: Profit and loss statements, balance sheets, and cash flow statements are essential for tax filing. These documents provide a snapshot of your business’s financial health and are necessary for accurate tax reporting.

- Consult with a Tax Professional: Meeting with a tax advisor or accountant can be invaluable. They can provide advice specific to your business situation, help identify additional deductions, and ensure that your filings are compliant with the latest tax laws.

- Check Deadlines and Compliance Requirements: Make sure you are aware of all relevant filing deadlines and compliance requirements to avoid penalties. This includes knowing when to file quarterly or annual reports and when payments are due.

- Plan for Tax Payments: If you expect to owe taxes, it’s wise to plan how you will cover these costs. This might involve setting aside funds throughout the year or arranging payment plans.

- Maximise Retirement Contributions: Contributions to certain retirement accounts can reduce your taxable income. Consider maximising these contributions before the end of the fiscal year.

- Review Employee Information: Ensure all employee information is accurate for payroll reporting, including social security numbers and addresses.

- Digitise and Backup Documents: Keeping digital copies of important documents helps you stay organised and also ensures that you have backups in case of data loss.

Why is Australia’s Financial Year from July to June? – FAQs

How does the tax year work in Australia?

In Australia, the financial or tax year runs from July 1 to June 30 of the following year. This period is used by individuals, businesses, and the government to calculate taxable income and assess tax liabilities. At the end of the financial year, taxpayers must submit their income tax returns, detailing their earnings and deductions over the past 12 months.

Do you have to do your tax every year in Australia?

Yes, all individuals and businesses in Australia are required to complete and submit a tax return every year. This annual process involves reporting income, claiming deductions, and ensuring the correct amount of tax has been paid. The deadline for individuals to lodge their tax return is generally October 31 following the end of the financial year.

Is tax paid monthly or yearly in Australia?

While the income tax itself is calculated and reconciled on a yearly basis, tax payments in Australia can occur more frequently. For example, employees have income tax withheld from their paychecks by their employer each pay period (e.g., fortnightly or monthly). Businesses may also need to make quarterly Pay As You Go (PAYG) instalments to the Australian Taxation Office (ATO) based on their projected income.

How often do Australians pay taxes?

Australians pay taxes regularly throughout the year. Employees have tax withheld from their wages by their employer with each pay cycle. Additionally, individuals who earn income from investments or run their own businesses may be required to make quarterly PAYG instalments. These regular payments help manage cash flow and ensure that taxpayers do not face a large lump sum payment at the end of the financial year.

Do you do your own taxes in Australia?

Many Australians choose to do their own taxes, using online platforms like myTax provided by the ATO, which simplifies the process. However, others opt to hire registered tax agents or accountants to prepare and lodge their tax returns, especially if their financial situations are complex or they want to ensure they maximise their deductions and credits. Using a tax agent can also provide an extended deadline for lodging the tax return.

Starting early and staying organised is key to managing tax time without stress. It’s always beneficial to maintain good habits throughout the year, rather than scrambling as deadlines approach. What that comes back to is your business mindset. Are you planning for 30 June now? Check out our End Of Financial Year Checklist For Business Owners.